In 2026, the global semiconductor industry is entering a transitional period as market structures and value chains realign to accommodate AI infrastructure expansion. The total market is projected to approach the $1 trillion mark, with memory semiconductors emerging as a key driver in terms of both demand and profitability. In particular, industry experts expect SK hynix to be the primary anchor of this shift, as a chipmaker capable of delivering both HBM3E and next-gen HBM4 reliably.

Growing Share of Memory Driven by AI Infrastructure Expansion

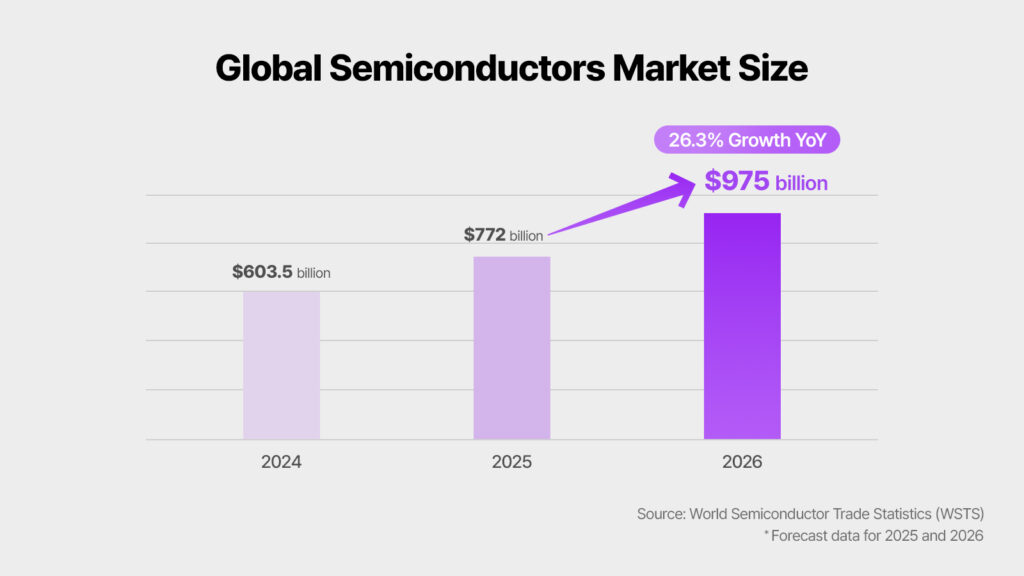

According to the World Semiconductor Trade Statistics (WSTS), the global semiconductor market will grow by more than 25% year-over-year in 2026, reaching approximately $975 billion, with the memory segment increasing at 30% growth. Market research firms and investment banks anticipate particularly high growth for server and data center memory, with some estimating the 2026 memory market size to exceed $440 billion.

Analysis suggests that as investments in servers for AI training and inference expand, the capacity of DRAM and HBM installed per server is steadily increasing. Simultaneously, demand for storage such as enterprise SSDs (eSSDs) is also rising, leading to a structural increase in the proportion of memory and storage within the overall AI infrastructure.

The Memory Supercycle and the Role of the HBM Market

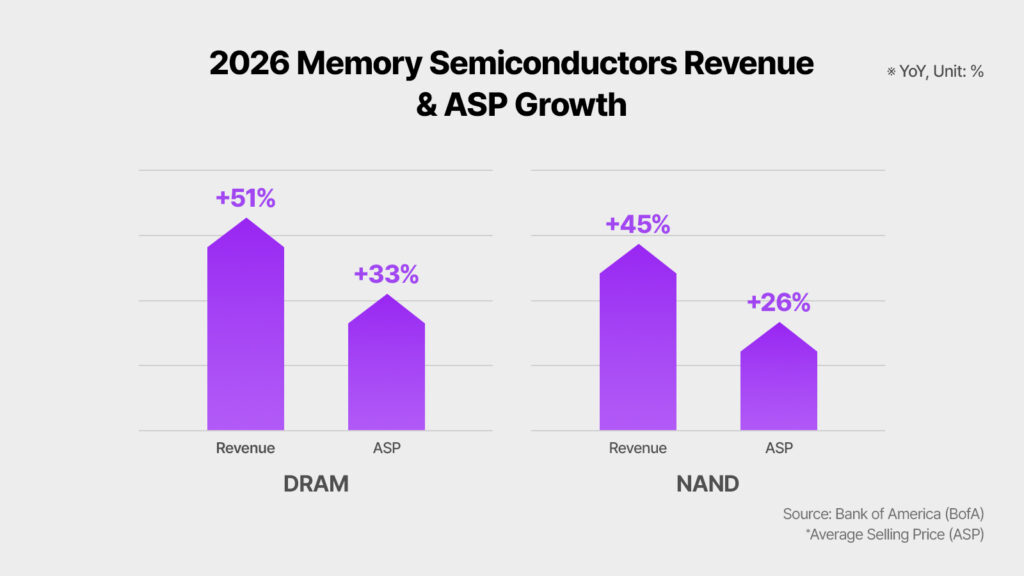

The term “supercycle” has been used in the industry to describe the strong momentum in the memory sector since 2024. The Bank of America (BofA) defines 2026 as a “supercycle similar to the boom of the 1990s,” forecasting global DRAM revenue to surge by 51% and NAND by 45% year-over-year, with Average Selling Prices (ASP) rising by 33% and 26%, respectively. Furthermore, BofA named SK hynix as the global memory industry’s “Top Pick,” predicting it will be one of the primary beneficiaries of this supercycle.

Global firms expect demand for AI-specific memory with HBM at the center to grow rapidly from 2025 to 2028. Some forecasts even suggest that the HBM market size in 2028 will surpass the entire DRAM market of 2024.

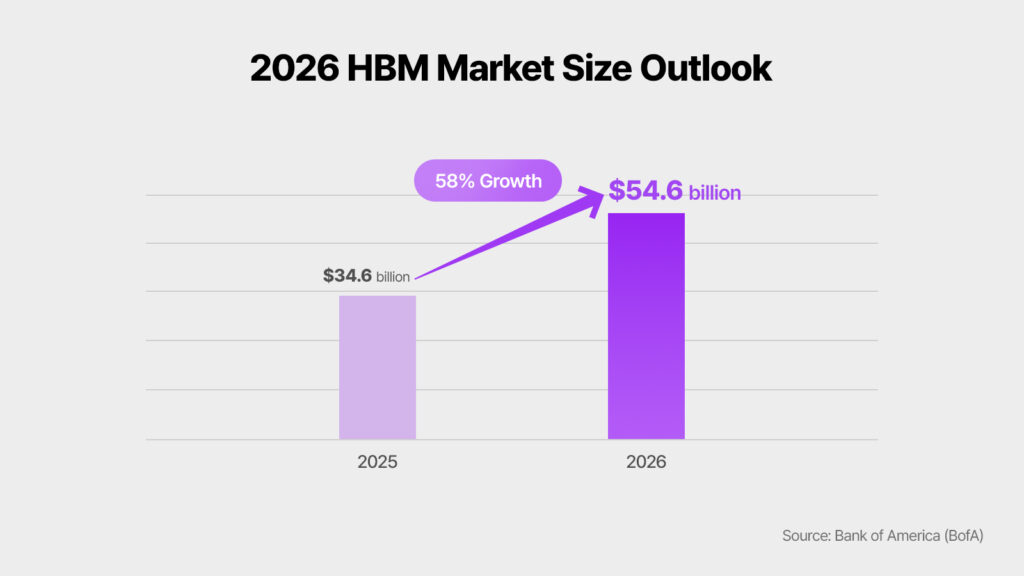

BofA estimates the 2026 HBM market to reach $54.6 billion, a 58% increase from the previous year. Goldman Sachs particularly forecasted that HBM demand for custom-ordered, ASIC-based AI chips will skyrocket by 82%, accounting for one-third of the market. This indicates that AI infrastructure investment is diversifying beyond general-purpose GPUs into specialized domains.

SK hynix’s HBM3E Leadership to Extend to HBM4

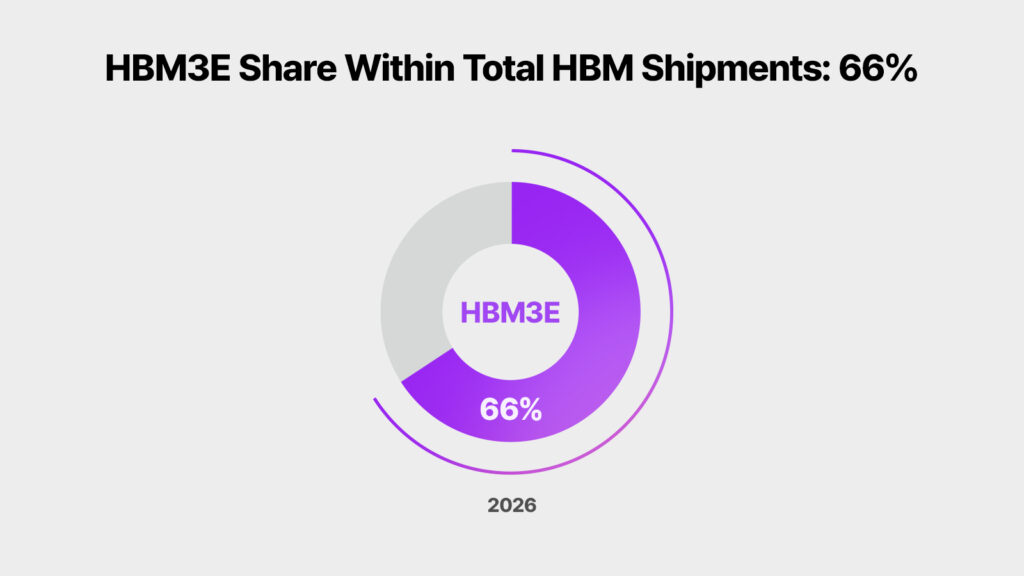

Most experts expect HBM3E to remain the flagship product in the 2026 HBM market. As NVIDIA did with their new “Blackwell Ultra” AI accelerators, Global Big Tech companies, including Google and AWS, are expanding their proprietary ASIC-based AI chip development and selecting HBM3E as the optimal solution. Major research and brokerage analysts expect HBM3E to account for approximately two-thirds of total HBM shipments in 2026, while HBM4 gradually increases its share.

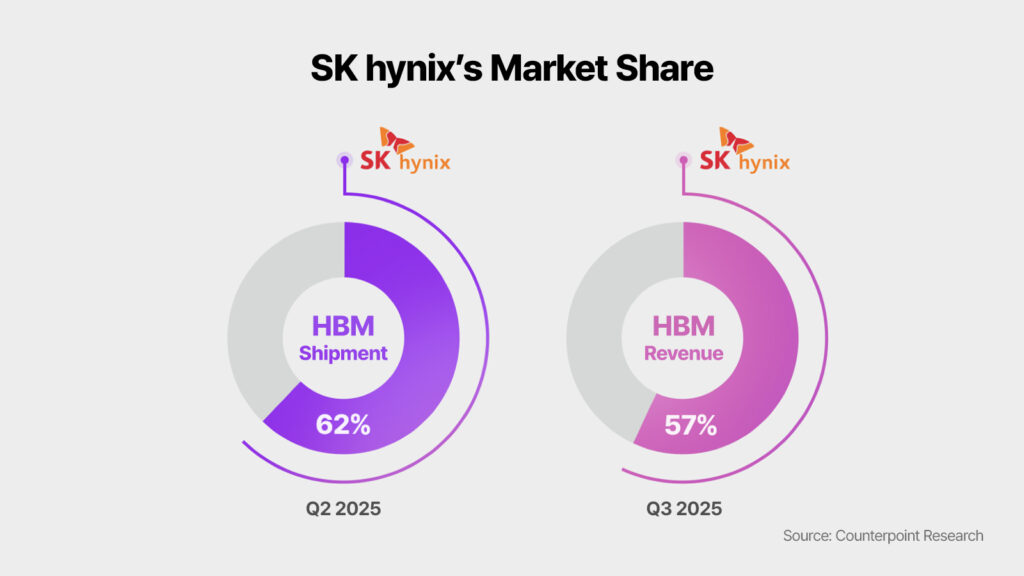

According to Counterpoint Research, SK hynix maintains a dominant position ranking No. 1 in the market with a 62% share of HBM shipments as of Q2 2025 and 57% of revenue as of Q3. Goldman Sachs assessed that “SK hynix will maintain its dominant position in HBM3 and HBM3E until at least 2026, sustaining a total HBM market share of over 50%.” UBS highlighted the company’s standing among Big Tech clients, noting that SK hynix will be the first HBM3E supplier for Google’s latest Tensor Processing Units (TPUs), the v7p and v7e.

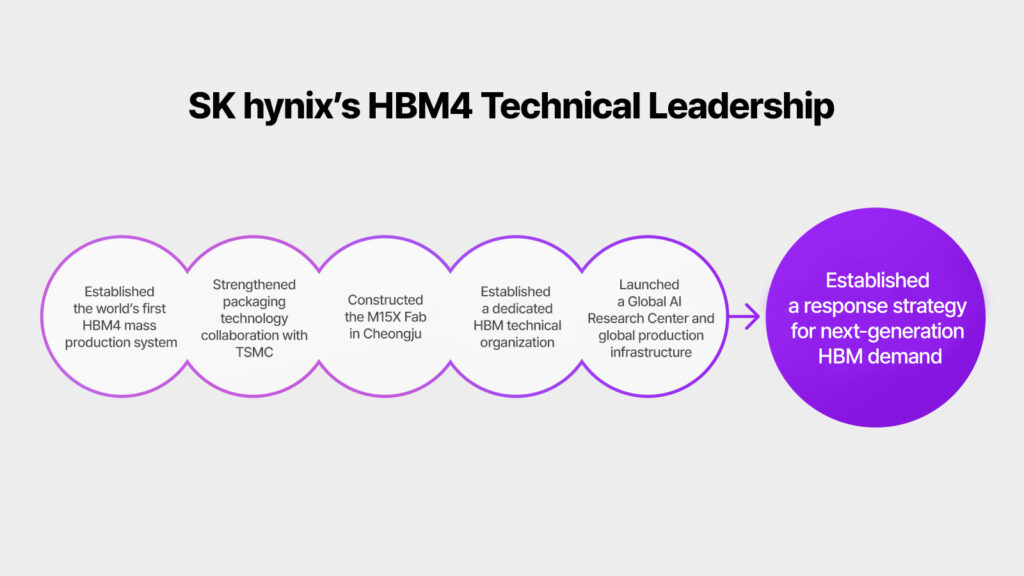

SK hynix’s leadership in HBM3E is naturally expanding to the next-generation HBM4. The chipmaker is already preparing for the market’s emergence, having secured the world’s first mass production system for HBM4 last September. The company has also finalized preparations to respond to growing AI memory demand by strengthening its packaging technology partnership with TSMC, building the Cheongju M15X fab, as well as establishing a dedicated HBM organization, a Global AI Research Center, and global production infrastructure.

As a result, SK hynix is expected to secure a unique competitive position by maintaining its market leadership in HBM3E while proactively establishing a development and supply system for HBM4, enabling it to fully support two generations of products by 2026.

UBS predicts that SK hynix will achieve approximately a 70% market share in the HBM4 market for NVIDIA’s next-generation Rubin platform in 2026. This suggests that its current leadership is carrying over to future technology generations.

Challenges Ahead – Price, Supply, and Geopolitical Risks

While the memory supercycle continues, cautious perspectives regarding price, supply, and geopolitical risks coexist. Some market researchers and overseas media suggest that HBM prices could enter a correction phase after 2026 due to intensified competition and expanded production capacity.

Additionally, increased DRAM production by latecomers and global semiconductor regulations are identified as variables that could affect the long-term market structure. However, the dominant analysis suggests a sudden shift is unlikely in the short term, as significant technical gaps remain in the high-performance HBM sector.

2026 Memory Market Outlook

Ultimately, the memory semiconductor market in 2026 can be viewed as a transitional phase in which the expansion of AI infrastructure, demand centered on HBM3E, and a gradual shift toward HBM4 are occurring simultaneously. HBM3E is expected to remain the primary memory used in AI servers and data centers, while major players including SK hynix are preparing for a smooth transition to the HBM4 generation based on the mass production experience and customer partnerships they have built with HBM3E.

Furthermore, focused investment in HBM is creating a virtuous cycle that improves profitability in the general-purpose memory market. As resources are diverted to HBM, the supply-demand balance for general DRAM is improving. Global institutional investors foresee that server DDR5 module demand will form the two main pillars of the DRAM market alongside HBM in 2026. NAND flash is also expected to grow next year, centered on eSSDs for AI data centers.

2026 is evaluated as the year when HBM3E leads the market as the golden standard, while HBM4 and general-purpose memory map out the mid to long-term growth trajectory. Industry experts and investment firms collectively emphasize that “HBM3E will still be at the heart of the market in 2026, and SK hynix will be positioned at the center of the AI memory supercycle.”