Competition surrounding AI semiconductors has entered a new phase—one that tests not only corporate capabilities but also national strategy and execution. Through this [Expert POV] series, we explore the opportunities and challenges facing the global semiconductor industry in the AI era from a range of perspectives, including technology, finance, policy, infrastructure, ecosystems, globalization, and sustainability.

The center of gravity in AI competition is shifting from compute to industrial infrastructure

Over just two years, from 2024 to 2025, the so-called “Magnificent Seven”1 companies invested more than $600 billion in AI. This wave of investment is expected to continue through 2026, and as investment in AI becomes increasingly concentrated, the role and requirements of computing infrastructure, particularly AI data centers (AIDCs), are evolving rapidly.

1Magnificent Seven: A term used to describe seven major U.S. technology companies—NVIDIA, Google, Amazon, Meta, Microsoft, Tesla and Apple. Borrowed from the classic Western film The Magnificent Seven, the label is commonly used to refer to a group of companies that have delivered exceptional market performance.

Until 2025, growth in the AI industry was largely driven by efforts to expand the capabilities of foundation models (FM).2 This led to massive investments in AIDCs built around high-performance parallel computing hardware, including GPUs and HBM. Beginning in 2026, however, AI is expected to expand more deeply into the physical world, diversifying into AI transformation (AX) models3 and vertical AI4 applications tailored to specific industries and domains.

2Foundation model (FM): A deep-learning model trained on broad datasets and designed to support a wide range of applications. Generative AI systems, including large language models (LLMs) such as ChatGPT, are representative examples of foundation models.

3AI transformation (AX) model: An approach that positions AI not merely as an automation tool but as a core driver of enterprise and industrial transformation, redesigning business processes and operating structures around AI.

4Vertical AI: AI systems trained and optimized using data and rules specific to a particular industry or domain, aiming to deliver greater accuracy and reliability than general-purpose AI.

Regardless of how AI applications evolve, semiconductors remain at the center of accelerating training, inference, and content generation within AIDCs. Competitiveness in the AI era will ultimately depend on semiconductor supply capabilities and the infrastructure that supports them.

The challenge is that only a limited number of companies and countries can manufacture and supply the advanced semiconductors required for AI. NVIDIA, which controls more than 90% of the AI GPU market, manufactures most of its products using TSMC’s leading-edge sub-4nm processes in Taiwan. The HBM required for these GPUs is supplied by only a handful of companies, including SK hynix.

As a result, the AI semiconductor supply chain remains concentrated among a small number of regions and companies. Expanding production capacity has become more than a corporate issue—it is increasingly a matter of national strategy. Ultimately, AI competition is expanding beyond the race to build larger models. The new challenge is determining who can secure the infrastructure required to operate those models reliably at scale.

How the expansion of AIDCs is reshaping semiconductor demand

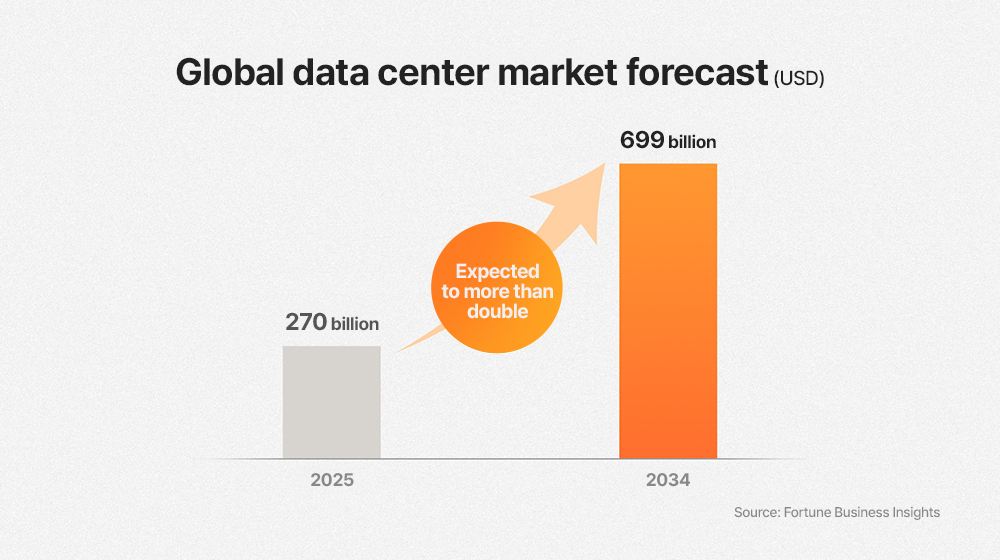

According to market research firm Fortune Business Insights, the global data center market was valued at approximately $270 billion in 2025 and is projected to reach roughly $699 billion by 2034[related link]. This growth reflects more than an increase in the number of facilities — it also signals the emergence of highly dense, power-intensive data centers optimized for AI computing as a core component of global industrial infrastructure.

At the same time, demand for general-purpose semiconductors used for data storage—including DRAM and NAND flash memory—is also expected to increase significantly. The expansion of AIDCs is therefore driving not only demand for specialized AI semiconductors, but also structural growth across the broader industry.

Against this backdrop, the role of memory companies is expanding beyond product supply to support the scalability of AI infrastructure itself. AIDCs require HBM for high-performance computing, DRAM for server and system operations, and NAND-based storage solutions for large-scale data storage and service deployment.

Competitiveness in the AI infrastructure era will therefore not be determined by the performance of a single product. Technology development, manufacturing capabilities, supply stability, and a portfolio that can meet evolving customer requirements must all work together. This is why global memory companies such as SK hynix play an increasingly important role in the AI ecosystem.

To supply memory semiconductors at the pace required by rapidly growing AIDC deployment, the industry must build large-scale semiconductor clusters commonly referred to as “megafabs.” However, developing such clusters is a challenge that extends beyond the capabilities of individual companies. Not only does capital expenditure (CapEx) for the construction of next-generation fabs far exceed that of previous facilities, but substantial investment is also required to build the surrounding infrastructure that supports these clusters.

As a result, leading semiconductor manufacturers are accelerating efforts to expand production capacity and secure infrastructure through collaboration with governments worldwide.

The competition for AI infrastructure is therefore for technology as well as execution. Success depends not only on developing faster and more efficient memory technologies, but also on building the manufacturing foundation, supply chains, and energy infrastructure necessary to produce and deliver them at scale.

Conditions for building successful semiconductor clusters

The success of semiconductor mega-clusters requires sophisticated industrial policies, including subsidies and timely infrastructure investment. Equally important is designing a framework that enables investments worth hundreds of billions of dollars to be deployed at the right time and at the necessary scale. It is also essential to establish financial and technological partnerships with major clients such as cloud service providers (CSPs),5 which require large volumes of memory semiconductors, while developing diversification strategies capable of responding to changes in the global value chain.

5Cloud service provider(CSP): An IT service provider that delivers cloud-based computing resources—including servers, storage, and networking—on demand via the internet. Representative examples include AWS, Microsoft Azure, and Google Cloud.

To maximize the value of semiconductor clusters, investment must extend beyond the manufacturing facilities to the broader infrastructure that supports them. Semiconductor clusters effectively function as large-scale social infrastructure, requiring substantial investment in power systems, industrial water resources, transportation networks, communications infrastructure, and port facilities. Among these requirements, securing reliable power and water supplies is particularly critical. Stable operation depends on transmission and distribution networks capable of delivering large amounts of electricity, as well as upgrades to power plants, substations, and grid infrastructure.6 Water resources and treatment facilities must also be expanded at the national level to ensure a reliable supply of industrial water.

6Grid: The interconnected system of power generation, transmission, and distribution infrastructure that delivers electricity from producers to end users

While constructing a megafab typically takes two to three years, building power transmission networks and power generation facilities can take anywhere from five to more than 10 years. For this reason, securing infrastructure must begin well before production facilities are completed. In addition, as AIDCs continue to expand, demand for cooling water is expected to rise significantly. Long-term investments in water treatment capabilities—including water recycling, wastewater processing, and alternative cooling technologies—will be essential.

Both AIDCs and semiconductor manufacturing are highly energy-intensive industries. AIDCs require enormous amounts of electricity to support large-scale computing workloads, while semiconductor manufacturing depends on a continuous and stable power supply to maintain process precision and product quality. As a result, power and water cannot be considered background infrastructure. They are critical factors that determine the pace of AI industry growth and the stability of semiconductor supply chains.

The energy bottleneck: A critical challenge for expanding AI infrastructure

As of today, “energy bottlenecks” in transmission and distribution networks have emerged as significant obstacles to becoming a leading AI nation. More precisely, the challenge is not necessarily a shortage of electricity itself, but rather the ability to deliver power when and where it is needed. This challenge extends far beyond the semiconductor industry and has become a common concern across many sectors in the AI era.

Leading U.S. AI companies developing large language models (LLMs) and foundation models are investing heavily not only in AIDCs but also in energy infrastructure. Microsoft Chairman and CEO Satya Nadella has noted that the company is unable to fully utilize available GPUs because of power supply constraints. To address this issue, Microsoft signed a 20-year power purchase agreement with Constellation Energy, the largest nuclear power producer in the U.S. Meanwhile, Amazon has partnered with Dominion Energy, and Google has signed an agreement with Kairos Power to support the development of small modular reactors (SMRs).7

7Small modular reactor (SMR): A compact nuclear reactor designed for modular manufacturing and on-site deployment. SMRs are considered a low-carbon energy source because they do not directly emit carbon dioxide during electricity generation.

Elon Musk’s xAI is focused on renewable energy, rather than nuclear power, and the company has built a solar power facility adjacent to its Colossus data center. While renewable energy currently represents a relatively small share of total data center power consumption, declining costs are expected to accelerate adoption of solar and wind energy across data center operations worldwide. As these examples demonstrate, competition among global Big Tech companies to secure energy resources is intensifying alongside preparations for the AI era. The semiconductor industry in particular is one of the largest consumers of electricity, and stable power supply remains essential to maintaining product quality. For this reason, securing reliable energy resources is likely to become the industry’s most pressing challenge.

This issue carries important implications for global stakeholders and industry participants alike. Expanding AI infrastructure requires more than simply acquiring additional GPUs and memory. It also requires the electricity needed to operate data centers, the manufacturing capacity needed to produce semiconductors, and the industrial foundation required to supply high-performance memory at scale.

Semiconductor clusters powered by electricity and water

Investment in power infrastructure must go beyond simply building additional power generation facilities. It must also support transmission and distribution networks capable of delivering large volumes of electricity reliably and on time, as well as the modernization and expansion of grid infrastructure. In addition, governments and industries should consider expanding investment in low-carbon energy infrastructure in response to evolving policy and regulatory frameworks, including Nationally Determined Contributions (NDCs),8the Carbon Border Adjustment Mechanism (CBAM),9 global carbon taxes,10 and broader ESG requirements.

8Nationally Determined Contribution (NDC): A country-specific climate action plan established under the Paris Agreement that outlines greenhouse gas reduction targets and implementation strategies.

9Carbon Border Adjustment Mechanism (CBAM): A regulatory framework, led by the European Union, that applies costs to imported products based on emissions generated during production, helping prevent carbon leakage and promote fairness in global climate policies.

10Global carbon tax: A policy approach that imposes taxes on carbon emissions as part of international climate action efforts. Various countries and regions use carbon pricing mechanisms to encourage emissions reductions.

Securing water resources is also emerging as a critical infrastructure challenge. The semiconductor industry consumes significantly more water than many other industries, including ultrapure water (UPW),11 for wafer cleaning and equipment operations. As demand continues to grow, existing water supply sources may no longer be sufficient, making reliable access an increasingly important operational risk.

11Ultrapure water (UPW): Highly purified water used throughout semiconductor manufacturing processes, including wafer cleaning and surface preparation. UPW is engineered to remove even nanoscale contaminants, helping improve yield and reduce defects.

AIDCs are also heavily dependent on water. Cooling systems and power generation processes associated with data center operations can require billions of liters of water annually. As a result, water security and water management have become structural challenges directly linked to the sustainability of both semiconductor manufacturing and AI infrastructure. Accordingly, long-term planning, along with systems for water reuse and recycling, will be essential.

Ultimately, the success of semiconductor clusters will not be determined solely by the technological competitiveness of individual companies. The key will be how effectively governments, local authorities, public institutions, and private companies work together to secure critical infrastructure—including electricity and water—before demand materializes.

The same principle applies to the global competition for AI infrastructure. No matter how advanced AI semiconductors become, AI deployment will remain constrained unless it is supported by sufficient capital, power, water resources, and manufacturing infrastructure. The semiconductor race in the AI era is therefore evolving beyond factories and equipment. Increasingly, success will depend on securing energy resources, critical infrastructure, supply chains, and execution capabilities at scale.

Memory at the center of AI infrastructure execution

As AI infrastructure continues to expand, the role of memory companies is broadening beyond product supply to support the performance and scalability of entire systems. AIDCs require multiple layers of memory to enable high-performance computing, server operations, large-scale data storage, and service expansion. In this environment, competitiveness depends not only on technology development but also on manufacturing capabilities, supply stability, and a portfolio capable of meeting diverse customer requirements. This is precisely why global memory companies such as SK hynix are critical within the AI ecosystem.

Ultimately, competition in AI can no longer be explained solely as a race among algorithms and models. To implement AI in real-world industries and services, computing performance, memory supply, data storage, power, water resources, and manufacturing infrastructure must operate together as a single integrated system. Beginning in 2026 and beyond, the focus of the AI industry is likely to shift from how large models can be built to how efficiently and reliably those models can be deployed and operated.

Success in the AI era will be determined by the combination of technological innovation to produce better chips and the execution capabilities required to manufacture and supply those chips at scale. At the center of that equation is memory infrastructure, which enables the movement, storage, and utilization of data across AI systems.

*This column was contributed by an external expert to provide insights into the AI semiconductor industry. The views expressed are those of the author and do not necessarily reflect the official position of SK hynix.