▲ Figure 1. One CIS is used per camera

The latest digital camera module used in smartphones generally consists of a CMOS image sensor (CIS), image signal processor (ISP), and dynamic random-access memory (DRAM). Among these, CIS is a semiconductor that reads the information of a subject and converts them into electrical signals. Originally, CIS struggled to compete with charge-coupled devices (CCD), but now courtesy of its improved performance, it is used widely across different industries, including smartphones and automobiles, based on its low-power characteristics and cost advantage.

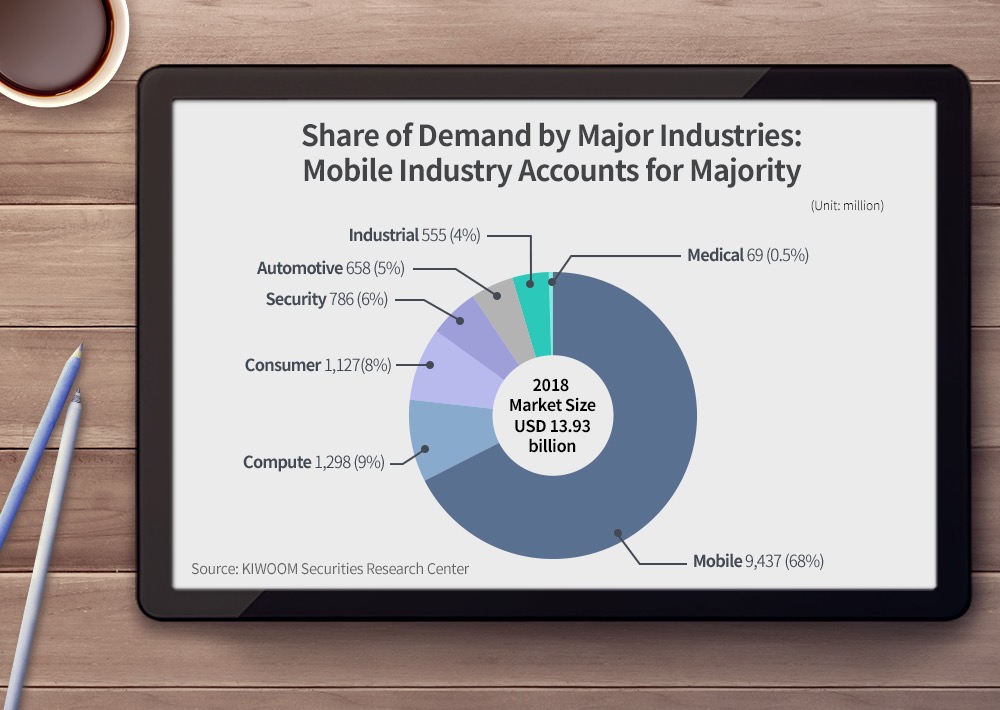

▲ Figure 2. Share of demand by major industries

As of 2018, the share of demand for CIS by major industries shows the mobile industry dominating at an unbeatable 68% – followed by compute (9%), consumer (8%), security (6%), automotive (5%), and industrial (4%). In the future, this demand is expected to grow mainly within the mobile, automotive, and industrial sectors, while the market’s size – which was valued around USD 13.7 billion in 2018 – is expected to increase to USD 19 billion by 2022.

The mobile sector, which holds the largest share by far, is expected to show the biggest growth as the number of multi-cameras equipped to smartphones increases. Triple cameras began to be adopted on the back of smartphones, after dual cameras. Considering the number of cameras on the front, now a total of five cameras can be equipped to just one smartphone as major smartphone manufacturers pursue new and diverse camera functions, like optical zoom, to differentiate their products in an extremely saturated market.

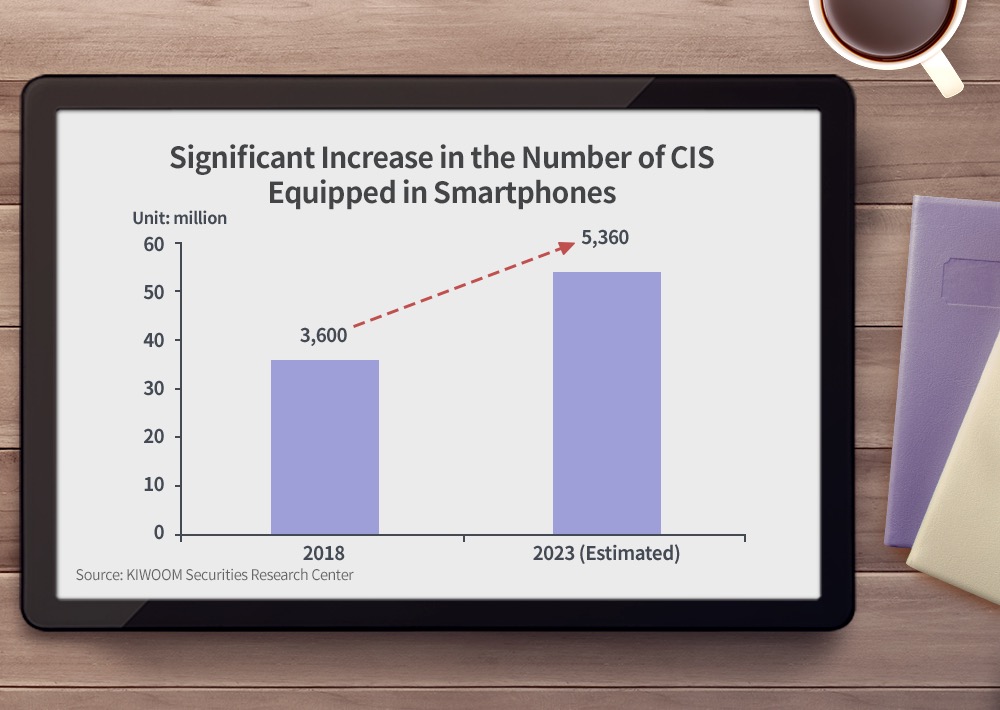

The number of cameras is expected to increase to provide more various functions such as augmented reality (AR), 3D simultaneous localization and mapping (SLAM* ), and real-time eye tracking. In fact, the number of CIS equipped in smartphones is expected to increase dramatically from 3.6 billion in 2018, to 5.4 billion in 2023.

▲ Figure 3. Significant increase in the number of CIS equipped in Smartphones

The front camera modules are becoming smaller and smaller with the recent increase in the adoption rate of full-screen displays. To achieve such a small size, the integration of CIS composed of color filters, photodiodes, and amplifiers is essential. The rear camera module is expected to develop in the direction of adopting special functions while raising the number of pixels. Especially, the pixel density has been increasing rapidly in recent, and for this, improving the pixel integration of CIS must be preceded. Therefore, the improvement of the integration level of CIS is becoming even more important for both front and rear smartphone cameras.

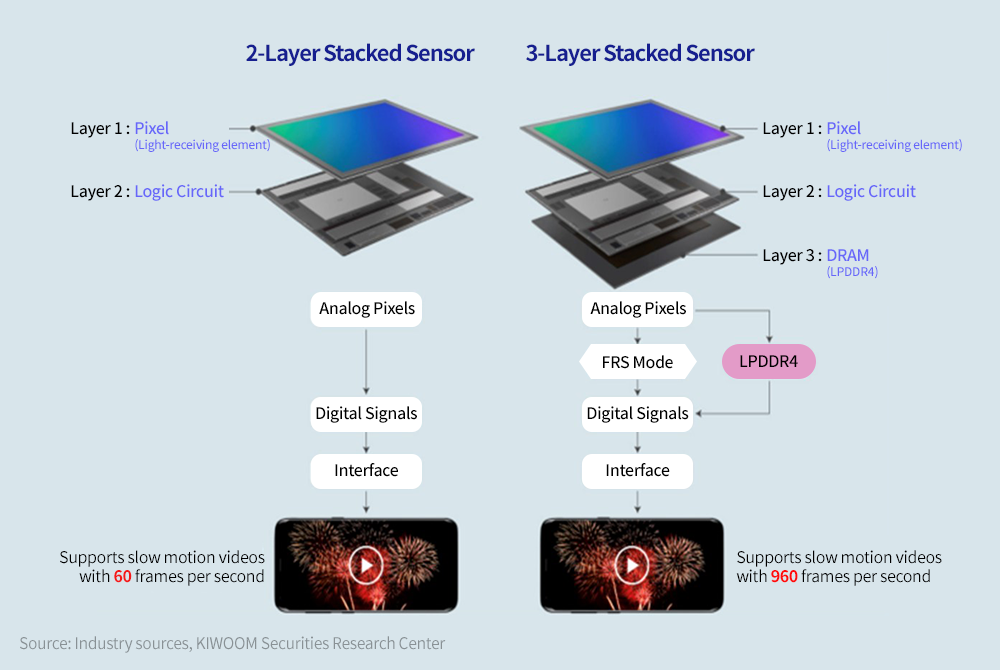

In addition to this, packaging technology integrating CIS, ISP, and DRAM is now being introduced to ultra-high-speed cameras, which is proving to be a beneficial change for companies producing both DRAMs and CIS in the mid to long term.

▲ Figure 4. Latest 3-layer (CIS + ISP + DRAM) stacked image sensor

For CIS, more demand for 12-inch wafers is being seen as focus shifts from 8-inch wafers. In addition, as the number of pixels increases to more than 40 million, the process started to move from 90nm to 32nm or less.

In particular, the manufacturing process of CIS is very similar to that of DRAMs, and the trench technology of DRAMs* is applied to the process of high-pixel products. Therefore, it is highly likely that DRAM manufacturers will have a cost advantage over time.

SK hynix is actually applying DRAM trench process technology to eliminate light interference between pixels, while several experiments are underway to prevent the absorption of photons when using metal partition walls. In addition, ISOCELL of Samsung Electronics has also adopted DRAM process technology and is making efforts to refine their process to a 32nm level.

SK hynix, and Samsung Electronics, two of the world’s leading semiconductor memory manufacturers, are expected to close the technological gap with leading CIS players such as Sony thanks to their superior DRAM technology.

SK hynix is currently operating 8- and 12-inch CIS lines. This year’s capacity of the 12-inch CIS line has increased by more than 60% compared to last year. In addition, since some lines are being redeployed for CIS, actual performance is expected to become more visible from the end of this year.

Samsung Electronics is also expanding the capacity of its 12-inch line in addition to its existing 8-inch CIS line, mainly by utilizing old DRAM lines. Starting with 11 lines in 2018, the company is planning to convert 13 lines into a CIS line in 2020.

The industry’s number one CIS manufacturer Sony continues to increase its 12-inch capacity in Japan, which is expected to intensify the competition for market share from the second half of this year. While Sony has to construct a new line, SK hynix and Samsung Electronics are converting and deploying existing DRAM lines, which would make their products highly competitive at cost, advantaging them in competition to secure market share.

* SLAM (3D simultaneous localization and mapping): A technology for constructing a map of surrounding environments by using attached sensors without any external help, which is extremely important for autonomous driving)

* SLAM (3D simultaneous localization and mapping): A technology for constructing a map of surrounding environments by using attached sensors without any external help, which is extremely important for autonomous driving)

※ This article is a reference material developed based on the subjective view of the contributor by utilizing materials and information trusted by KIWOOM Securities Research Center, and its accuracy and integrity cannot be guaranteed. Decisions regarding the trade of securities should be made entirely by the investor’s judgment, under the investor’s responsibility. KIWOOM Securities Research Center does not take any responsibility for the results of any investment actions made in accordance with the content of this article.

By Yuak Pak

Analyst at KIWOOM Securities

※ This article is based on the subjective view of the contributor, and may differ from the official stance of SK hynix.